Is Using Savings to Pay off Debt Right for You?

If you want debt advice, read this article, and you will get the best things that I learned over the past five decades to help you navigate debt. I have been through it all, from being very wealthy to going bankrupt and back up again. I am happily semi-retired with no worries about finances or anything else at this time of my life. I use all the earnings from writing articles like this one for charitable work. I especially like taking care of abandoned dogs and older adults in the community where I live. Do you know why dogs are always happy? There is no such thing as a doggy credit card.

You will get it straight from my life’s experiences about what you can do, especially if you are a young person just starting in your adult life. But, even if you are older, there are many things to consider about managing money.

When I was younger, for accounting processes, we did everything on paper or using spreadsheets. Now, there is an excellent system to manage finances on the Goalry Mall that I highly recommend. This system is almost fun to use, like playing a game of Monopoly® or something like that.

Three types of savings are important:

- Saving for an emergency fund

- Saving for retirement

- Saving to buy a home

Let me be clear, when I use the word “savings,” I do not mean putting U.S. dollars in a bank account. That is the worst thing you can do. That is no longer a good option.

First, Some Economic Terms and Definitions

To understand what happens to cash, we need to discuss a few concepts first. Let me explain.

Inflation

Inflation is a hidden cost that reduces the value of holding cash. For example, if last year you bought a candy bar for $1, inflation may cause the price this year to increase to $1.05. Also, manufacturers can reduce the portion size to hide inflation by making your candy bar 5% smaller and charge the same price for less.

I once bought a package of potato chips that were marked on the package as having more. When I opened the package, it was filled with more air, and the few chips that fell out seemed like a complete ripoff. The potato chips were in a big bag filled with air. If I wanted a balloon, I would have bought one instead of the chips. To avoid this problem, check the net weight on the package to see if it is the same as before.

Consumer Price Index

The consumer price index (CPI) is the “official” published index about inflation in America. However, it is subject to manipulation by the Bureau of Labor and Statistics, the organization that chooses the bundle of goods used to calculate the CPI.

The choices for the goods to be tracked for price changes are controversial. At best, the CPI is a lagging indicator of past inflation. Therefore, it is very likely the true inflation rate is underreported. For example, the current CPI is 2.67%. This means your cash buys 2.67% less this year than it did last year.

Devaluation of the U.S. Dollar

The loss in value of the dollar over time is what economists like to call “invisible inflation.” It happens slowly, so it is not so obvious. The dollar goes down in value based on the inflation rate and the amount of money in circulation.

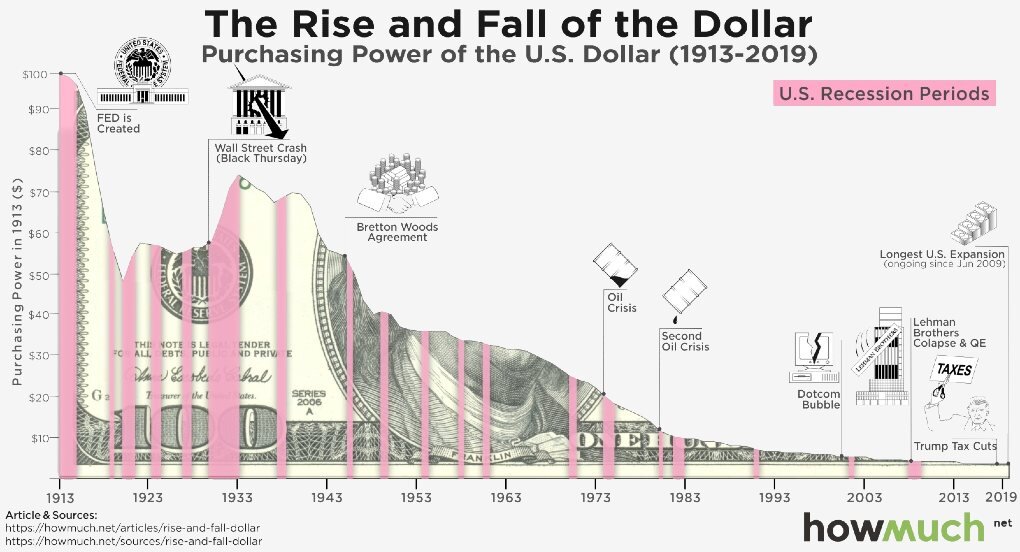

Since the Federal Reserve formed in 1913, the U.S. dollar lost 96% of its purchasing power. Howmuch.net has a chart that shows this erosion of the value of the U.S. dollar.

The chart shows that $100 in 1913 would buy only $3.87 worth of goods in 2019. In 2020, the Federal Reserve (FED) created an additional $3.38 trillion, which represents an increase in the money supply by 18%. This move by the FED took approximately another 18% of the value away from the U.S. dollar.

Be sure you understand that the FED is not a government agency. It is a private corporation owned by banks. The FED forces the U.S. government to borrow money and pay interest to the bank to pay for deficit spending. The U.S. issues T-Bills, and the FED and others purchase those as debt obligations of the U.S. government.

It may surprise you to hear that the FED operates at a profit each year for its owners and has a built-in annual dividend of 6% for its owners. The FED creates money out of nothing and makes a profit lending the fiat money to the U.S. government. Fiat money has no assets such as gold, backing it up with something of real value.

Ponzi Scheme

Many call this a Ponzi scheme, which causes the federal debt to continue to rise with no possibility of ever paying it. In essence, America has been sold to the bankers, and they gave nothing for it besides some accounting entries.

If you check the interest rates paid by bank accounts for savings, they are about half of one percent now. That is why it is not attractive to put any money in a savings account at a bank. However, other much more beneficial ways exist to create savings that are better choices when compared to placing money in a bank account.

Debt Elimination

You might think that getting rid of all debts would be a great idea. Not really, because without debt, you could not finance anything like a house or a new car. The only common way that most people get rid of nearly all debts is to file bankruptcy. That is something you want to avoid.

Is using savings to accomplish debt elimination right for you? The key is to manage your debts using easy-to-use online tools like Debtry.

Emergency Cash

Before you pay off debts, make sure you have emergency cash on hand. I call this the Bank of the Glass Jar. Go to the bank and get new currency bills in low denominations, some $20s, $10s, $5s, and $1s. Put this cash money in a glass jar. Have at least one month’s of emergency food money in cash. Three months is better.

Over time the cash will continue to use value. However, this cash can be used if all the systems fail to operate. For example, in a natural emergency, the ATMs and credit card transactions may not work if the communication systems go offline or there is a power outage.

Store this emergency cash in a fire-safe box. Put it in a secure location that is easy to get to in the case of a serious emergency. Only tell your closest, most-trusted, loved ones where you keep this money, or don’t tell anyone at all.

If you find yourself in an emergency and you don’t have any cash, use Cashry to get ideas of what you can do for a short-term cash crisis. If you have your emergency funds and still have extra cash left over, then take these next steps.

Evaluate Your Use of Credit

Using credit wisely it’s the key to building wealth. But, unfortunately, things that people do wrong, which get them into trouble, are spending more than they can afford, using high-interest credit cards, not paying them off, and not saving for retirement.

After you have your emergency cash in a glass jar, you want the next action to pay off all your high-interest credit card accounts. You can also consider a consolidation loan to pay off the high-interest credit card accounts.

Credit History

Use the online tool, Creditry to manage your credit history and improve your credit score. Having a good credit score will get you the best interest rates on the loans that you take. Wealthy people get the best offers for loans and credit card rates when they maintain an excellent credit score.

What is my FICO score?

You are allowed one free annual credit report from annualcreditreport.com and anytime you are turned down for a loan.

The FICO score is your credit score, and it is a number that ranges from 300 to 850.

550 or below is considered bad, and the level of the score from personal bankruptcy.

551 to 669 are considered fair scores yet make loans more costly.

670 to 739 are considered good scores and results in better deals on loans.

740 and above is considered excellent and gets the best rates available for most loans.

Find Refinance Options. Deal with Your Debt.

Meet Debtry.

Savings That are Not Cash

Many people do not realize that savings can be done by using assets other than cash. Examples include storing gold or silver. Those who save gold or silver coins are called “stackers.” This is because these precious metals held value over time compared to the erosion of the value that occurred for the U.S. dollar.

In 1915, a couple of years after the FED started, one ounce of gold was worth around $19. In May 2021, one ounce of gold is worth around $1,900, showing a return of about 100 to one over the past 106 years. This is the same as if you earned 4.4% interest each year for the past 106 years.

Keeping gold was much better for preserving value than stuffing U.S. dollars in a mattress. The same thing happens with collecting silver. However, you do have to be careful with holding physical gold or silver that it does not attract thieves, and it should be insured against loss.

Investing for Retirement

If you are a young person, you should consider using the tools at Goalry to set up a plan to build retirement funds. First, make a monthly budget using Budgetry and include putting aside something for retirement as part of your monthly budget.

Helpful Tip: Stop spending $5 per day on a gourmet coffee or another wasteful expense. Instead, put $150 per month away in your retirement account.

IRA

Savings for retirement is also about saving taxes. An investment retirement account (IRA) allows you to fund up to $6,000 for your IRA in 2021 ($7,000, if you are older than 50 years old).

Here is how you do this.

Open an IRA investment account at an online brokerage that does not charge any fees.

Automatically fund the account with $500 each month to use the maximum tax-deferred funding level allowed.

Use the investment method of dollar-cost averaging to invest in stock monthly.

For your stock picks, choose companies that are long-term “value” creators, which pay a dividend. Then, choose to automatically reinvest the dividends. These are major international brand name companies that make profits despite any economic changes. An example would be Kraft Heinz. If you need some further good hints about the companies to buy, review the holdings of Berkshire Hathaway.

Hold the shares you buy until retirement as a “buy-and-hold” strategy.

Upon retirement, you can take withdrawals from the IRA account and pay taxes on the withdrawals. Presumably, you will be at a lower tax rate when you are past retirement age.

You can make withdrawals from an IRA starting at age 59 1/2. If you make any withdrawal before that time, there is a 10% penalty. You must start withdrawals at age 70 1/2 or 72, depending on your birthday.

The goal of saving for retirement is to let your value stocks appreciate and increase the compounding effect by re-investing the dividends. You will do well if you continue to do this consistently each month. The 20-year average annual returns from the S&P 500 range from 5.90%, up to 13.6%, with some years being losers.

How Much Will You Have for retirement?

Let take a very encouraging example and calculate how much money can be saved for retirement.

Imagine you just got out of college, and you got your first job. You are elated, and you deserve to celebrate. But, first things first, if you are living with your parents, do not rush to move out of their house until you have enough money to save $500 per month.

Many young people want their freedom so badly that they move out and have to pay rent. It is better to take a job being a maintenance person or an apartment manager in exchange for a free place to stay than to pay rent. If you pay rent, you make the landlord rich, which is not a good strategy for building wealth.

If you pay no rent or as little rent as possible, at the age of 22, you can start saving $500 per month in an IRA, which is invested in value stocks, for your retirement.

Let’s use the average S&P return of 10%, which should be your investment goal. Imagine you work until the age of 70 before taking any withdrawals. That is 48 years.

At age 70, you will have $7,096,538.

If you live until the age of 100 years old, you can take $19,712 per month to live on before you run out of money if you wait until you are70 to start making withdrawals. Even so far in the future, that amount should be enough to have a nice life.

Conclusion

Is using savings to pay off debt right for you? The answer is yes if you have enough emergency cash put away. After you have your emergency fund, you do with any extra cash to pay down any outstanding credit card balances that are wasting your money paying high interest rates. Get rid of those outstanding balances, and start paying yourself to build your future wealth for a happy retirement. Don’t forget to use all the online tools at the Goalry Mall to make building your wealth easier.